How to calculate product cost: Concepts and legal basis you need to know

19-09-2025 745

Product cost is a synthetic indicator reflecting the results of using assets, materials, labor and capital in the production and business process, reflecting the cost management results of the enterprise.

Concept of product costing

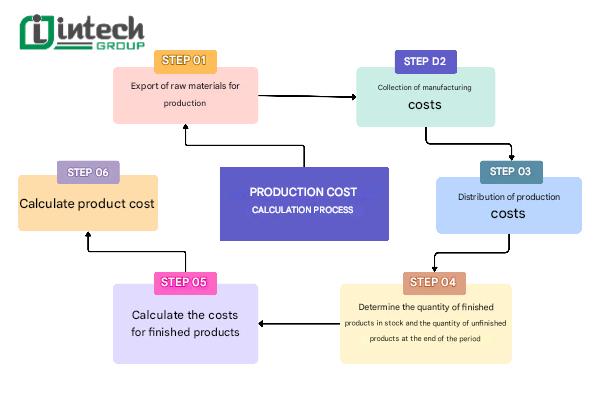

Product costing is an important step that helps businesses determine the total costs required to produce a complete product unit. This is the basis for setting selling prices, controlling costs and evaluating the effectiveness of production and business activities. According to Circular 133/2016/TT-BTC and Circular 200/2014/TT-BTC, product costing is the sum of all direct and indirect costs such as:

- Direct material costs (including main and auxiliary materials),

- Direct labor costs,

- General production costs (depreciation, tools, electricity, water, workshop management salaries, etc.).

Mastering the costing method not only helps businesses ensure compliance with legal regulations, but also optimizes financial management and enhances competitiveness in the market.

Classification of product costing

In the process of learning how to calculate product costing, cost classification is an important step to help businesses optimize product costing and choose appropriate cost management methods. Below are two common classification methods:

1. Classification of product costing by calculation time

- Planned costing: Is the cost level estimated in advance based on the quantity of products and production costs according to the set plan.

- Standard costing: Is established based on economic and technical standards at a specific time in the planning period.

- Actual costing: Is the costing determined after completing production, based on actual cost data recorded by the accounting department.

2. Classification by costing scope

- Production costing: Includes direct costs incurred in the workshop such as raw material costs, direct labor and general production costs.

- Cost of sales: Broader than production cost, including business management costs and sales costs to bring products to consumers.

The importance of determining the right way to calculate product cost

Choosing the right way to calculate product cost helps businesses accurately determine the total cost to complete a product. This is not only the basis for setting a reasonable selling price, but also helps businesses build a competitive plan, optimize production costs, and improve financial management efficiency. Understanding and applying the right way to calculate cost will help businesses control costs well and improve competitiveness in the market.

Product pricing method

1. How to calculate product cost by simple method (direct method)

Among the ways to calculate product cost, the simple method, also known as the direct method, is a suitable choice for businesses with simple production models, closed processes, few product types, and large-scale production in a short time.Applicable characteristics:

- Businesses only produce one or a few types of products.

- Continuous and stable production process.

- Short production cycle, products completed quickly.

- There are few or no unfinished products at the beginning and end of the period.

Cost calculation formula:

| Total production cost = Unfinished production cost at the beginning of the period + Production cost during the period - Unfinished cost at the end of the period |

For example:In June, Intech Group Company produced product A, in which the costs incurred are aggregated related to the production process of product A as follows:

- Total cost for direct materials: 600,000,000 VND;

- Total cost for direct labor: 70,000,000 VND;

- Total cost for general production: 90,000,000 VND.

Intech Group Company has no unfinished products at the beginning and end of the period. All 76 products A are transferred to the warehouse after completion. Calculate the cost price of product A:

Solution:- Total cost of production of product A = 600,000,000 + 70,000,000 + 90,000,000 = 760,000,000 VND;

- Unit cost of product A = 760,000,000/76 = 1,000,000 VND.

2. How to calculate product cost by standard method

This is the optimal choice for businesses that have a stable production process and a tight management system. This method helps to control costs effectively and promptly detect deviations in the production process.

The standard method is often applied to businesses with a clear and stable production process that have established detailed cost norms for each production stage. In addition, there is an accounting system capable of calculating, monitoring and adjusting norms regularly.

Timely detect waste and deviations in the use of raw materials, labor and general production costs.

Costing formula:

| Actual product cost = Standard cost per unit of each product type * Cost ratio (%) |

In which:

| Cost ratio (%) = (Total actual production cost of all products / Total standard production cost of all products) x 100 |

3. How to calculate product cost by coefficient method

This method is commonly applied to businesses that produce many different types of products from the same technological process. The outstanding feature of this method is that costs are aggregated for the entire production process, then reallocated to each type of product according to the conversion coefficient.

Subjects to apply the coefficient method:

This method is suitable for businesses that have the characteristics of using stable raw materials and labor, not changing much between periods, obtaining many products at the same time from the same technological process and cannot separate costs for each type of product, because they are created at the same time.

Some industries that often apply this method include: Garment, chemical processing, mechanical and electrical manufacturing, livestock and agricultural processing, processing, manufacturing of diverse products from a single source of input materials.

Cost calculation formula:

| Standard unit cost of a product = Total cost of all products / Total number of original products |

In which:

| Number of standard products = Number of products of each type x Conversion coefficient of each type |

For the conversion coefficient, the enterprise needs to determine separately for each different type of product on a product type. The conventional standard coefficient is coefficient 1.

| Total cost of product production = Number of standard products x Unit cost of standard product. |

For example:

A consumer goods manufacturing company has a simple and closed technological process. During the period, the enterprise produced two types of products, X and Y. The cost conversion coefficient has been determined: product X coefficient: 1, product Y coefficient: 1.5

- Unfinished costs at the beginning of the period:

- Direct materials: 100,000,000 VND

- Direct labor: 30,000,000 VND

- General production costs: 40,000,000 VND

- Costs incurred during the period:

- Direct materials: 300,000,000 VND

- Direct labor: 60,000,000 VND

- General production costs: 90,000,000 VND

- Costs incurred during the period:

Completed production of 100 products X, 60 products Y. Unfinished product output: 30 products X (50% complete) and 20 products Y (50% completed). Calculate the cost of products X, Y according to each item in which the cost of raw materials arises once from the beginning of the technological process, other costs arise gradually. Solution:

Solution:

- Total number of finished products according to standard products: 100 x 1 + 60 x 1.5 = 190

- Total number of unfinished products converted to allocate raw material costs: 30 x 1 + 20 x 1.5 = 60

- Total unfinished products converted to allocate processing costs (direct labor, general production) = 30 X × 1 × 50% + 20 Y × 1.5 × 50% = 30.

- Allocating costs according to total output:

- Total cost for direct materials: {(100,000,000 + 300,000,000) / (190 + 60) × 60}/ (250 × 60) × 60 = 57,600,000 VND

- Total cost for direct labor: {(30,000,000 + 60,000,000) / (190 + 30) × 30}/ 220 × 30 ≈ 12,272,727 VND

- Total cost for general production: {(40,000,000 + 90,000,000) / (190 + 30) × 30}/ 220 × 30 ≈ 17,727,273 VND

- Calculate the total cost of standard products in the period:

- Raw materials: 400,000,000 – 57,600,000 = 342,400,000 VND

- Direct labor: 90,000,000 – 12,272,727 = 77,727,273 VND

- General production cost: 130,000,000 – 17,727,273 = 112,272,727 VND

+ Total converted cost of finished products: 342,400,000 + 77,727,273 + 112,272,727 = 532,400,000 VND

+ Total cost of Product X (100 products, coefficient 1): Cost = 532,400,000 / 190 × 100 ≈ 280,210,526 VND

+ Total cost of Product Y (60 products, coefficient 1.5): Cost = 532,400,000 / 190 × 1.5 × 60 = ≈ 251,578,947 VND

4. How to calculate product cost by order method

The method of calculating by order is a suitable choice for businesses that produce according to customers' specific requirements. This method ensures high accuracy because all costs are recorded and allocated specifically to each order.

Applicable subjects:

The method of calculating costing by order is suitable for businesses that produce single items, small batches, or customized products. Industries with production processes according to individual orders such as: mechanical engineering, shipbuilding, interior design, printing, electronic equipment manufacturing, etc.

Characteristics of the method:

- Costs are determined separately for each order.

- Costs of raw materials, labor, and general production costs are all directly collected or allocated in detail for each order.

- Requires a tight accounting system, recording costs according to the order production progress.

Costing formula:

| Cost of each order = Total direct material cost + Direct labor cost + General production cost (*) |

(*): These costs are calculated from the beginning to the end of the order.

5. How to calculate product cost by step method

This is the optimal choice for businesses with complex production processes, divided into many consecutive stages or workshops. Each production stage can generate its own costs and be closely monitored and controlled.

Applicable subjects:

The step method is suitable for businesses with production processes consisting of many consecutive stages, wishing to collect costs and calculate costs by each department or workshop, with high internal accounting needs between production stages or selling semi-finished products to the outside.

Some commonly applied industries: Food processing industry, pharmaceutical production, multi-stage mechanical processing, chemicals, metallurgy...

Characteristics of the method:

- Costs are collected separately for each stage or production department.

- Businesses must calculate the cost of semi-finished products after each stage before moving on to the next step.

- The final cost of a finished product is the total cost of all steps added together.

Calculation formula:

| Cost of finished products in the period = Cost of products in stage 1 + Cost of products in stage 2 + …. + Cost of products in stage n |

6. How to calculate product cost by the method of excluding by-products

In the process of learning how to calculate product cost, the method of excluding by-products is the method applied in cases where the enterprise simultaneously obtains main products and by-products from a production process.

Applicable subjects:

The method of excluding by-products is suitable for enterprises operating in: Chemical industry, food processing, mineral exploitation, agricultural and forestry processing

Characteristics of the method:

- All initial production costs are collected for both main products and by-products.

- Then, the value of the by-product will be determined and excluded from the total production cost, in order to accurately reflect the cost of the main product.

- Determining the value of the by-product can be done in many flexible ways depending on the characteristics of each enterprise.

Cost calculation formula:

| Total cost of main product = Value of unfinished main product at the beginning of the period + Total costs incurred during the period - Estimated value of recovered by-product - Value of unfinished main product at the end of the period |

Guidelines for accounting for the collection of production costs according to Circular 133

One of the important factors in calculating product cost is the accounting for the complete and accurate collection of production costs. Below is the method of cost accounting according to Circular 133, especially the way to account for costs incurred during the production process, including enterprises applying automated production lines in modern production.

- Direct material costs, based on production warehouse receipts for accounting

- Debit account 154 - Credit account 152, 153: Value of raw materials issued to warehouse

- Salary costs and related compulsory insurance costs, based on salary and insurance receipts

- Debit account 154 - Credit account 334, 3383, 3384, 3386.

- General production costs: General production costs include depreciation of machinery, allocation costs of tools and equipment, outsourcing costs such as electricity and water, processing, etc.

Credit account 214: Depreciation costs of machinery and factory

Credit account 242: Allocation of tools and equipment

Credit account 335 / 111 / 331: Outsourcing costs, electricity and water, processing services, etc

- Accounting for raw materials returned to warehouse due to not being used up, based on the warehouse receipt.

- Debit account 152 - Credit account 154: Value of re-imported raw materials

- Accounting for production costs exceeding the allowable norm.

- Debit account 632 - Credit account 154: Production costs exceeding the norm.

- Accounting for completed finished products:

- Debit account 155: Value of finished products in warehouse;

- Debit account 632: If the finished product is not in warehouse but sold directly (usually applied to construction or service activities);

- Debit account 241 / 642, 641: If the finished product is not in warehouse but put into immediate consumption;

- There is account 154.

Answers to frequently asked questions about product costing

In the process of applying product costing methods, especially when the enterprise has deployed an automated production line, there are many accounting operations and cost aggregation methods that need to be clearly understood. Below are some questions to help you better understand the process of calculating and evaluating products in production.

1. What methods do businesses often use to evaluate unfinished products?

Unfinished products are products that are not completed at the end of the period. Correctly evaluating the value of unfinished products directly affects the accuracy of calculating product costs. Commonly applied methods include:

- Method 1 - According to the cost of main raw materials

Evaluate unfinished products based on the direct raw materials used during the period.

- Method 2 - According to equivalent products

Estimate unfinished products based on the actual level of completion (by percentage), then convert them into equivalent finished products.

- Method 3 - According to standard costs (plan)

Applied when the business has established production cost standards for each stage, helping to control unfinished costs more effectively. For businesses with automated production lines, methods 2 and 3 are often preferred due to their high accuracy and ease of extracting data from the automated system.

.jpg)

2. The process of collecting production costs in a period and how to collect costs by object?

To ensure the accuracy of the costing process, businesses need to organize a suitable accounting system, track costs by period and by production object. Specifically:

- Inventory accounting method:

- Regular declaration: Continuously record all import and export transactions during the period, suitable for large-scale businesses applying high technology.

- Periodic inventory: Conduct inventory and determine costs at the end of the period, suitable for small businesses or batch production.

- How to collect costs by object:

- According to the entire production process: Applied when businesses produce in large quantities.

- By product, order or job: Suitable for single-piece production, according to order.

- By group, team or production stage: Applied in businesses with automated production lines, helping to control detailed costs according to each technology segment.

Understanding the methods of evaluating unfinished products and the process of collecting production costs is an important step in calculating accurate product costs. Especially for businesses applying automated production lines, combining cost accounting and data from automated systems will help optimize production management, save costs and improve financial efficiency. For any questions, please contact Intech Group for advice and support.